Correlation analysis between cryptocurrencies and traditional financial markets

Mingkai Liu

Co-Presenters: Individual Presentation

College: College of Business and Public Management

Major: Accounting

Faculty Research Mentor: Huaibing Yu

Abstract:

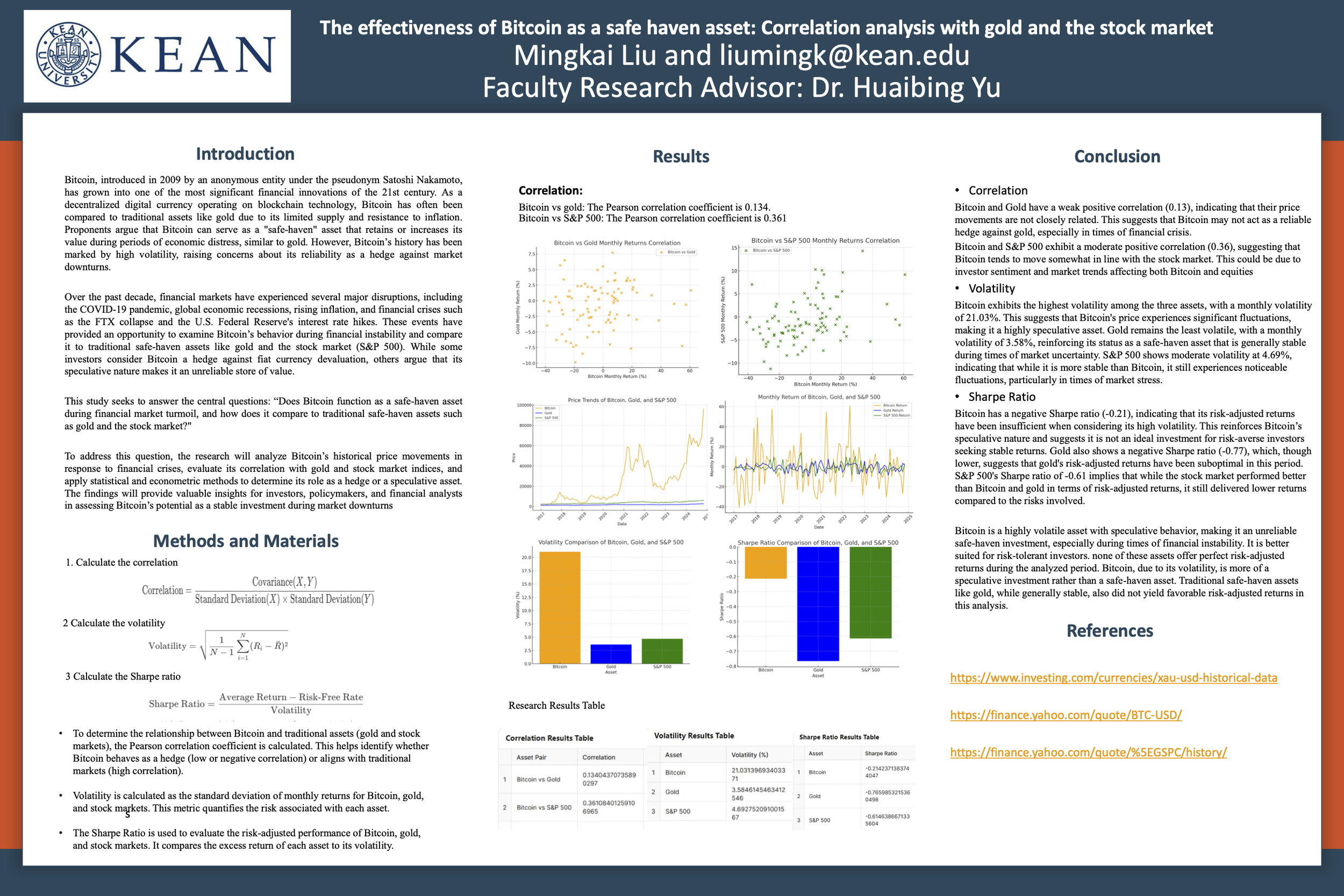

This study examines the role of Bitcoin as a safe-haven asset during periods of financial market instability and compares its performance to traditional assets such as gold and the S&P 500. Bitcoin, introduced in 2009, has gained significant attention due to its decentralized nature and resistance to inflation, yet its high volatility has raised concerns about its reliability as a store of value. In contrast, gold is widely regarded as a safe-haven asset, and the S&P 500 represents a broad market index.By analyzing the historical monthly price movements and returns of Bitcoin, gold, and the S&P 500 during periods of market disruptions, such as the COVID-19 pandemic and other economic crises, this study investigates the correlation between these assets, their volatility, and their risk-adjusted returns (Sharpe ratio). The results reveal that while Bitcoin exhibits high volatility and a weak correlation with gold, it shows a moderate correlation with the S&P 500. Furthermore, Bitcoin's risk-adjusted returns, as indicated by a negative Sharpe ratio, suggest that it has not consistently served as a reliable safe-haven asset.he findings highlight that Bitcoin, though sometimes correlated with traditional financial markets, behaves more like a speculative asset than a safe-haven investment. Gold, while less volatile, did not offer optimal risk-adjusted returns during the analyzed period. The S&P 500 provided moderate returns, but its volatility remains a concern. This research provides valuable insights for investors, policymakers, and financial analysts in assessing Bitcoin's potential as a stable investment during times of market turmoil.