Portfolio Optimization under ESG and Constraint Settings: Markowitz Model vs. Index Model

Jiatong Han

Co-Presenters: Yao Xiao, Kai Yun, Yixin Zou, Yashu Ji

College: College of Business and Public Management

Major: BS.ACCOUNTING

Faculty Research Mentor: Wei Chun Zhu

Abstract:

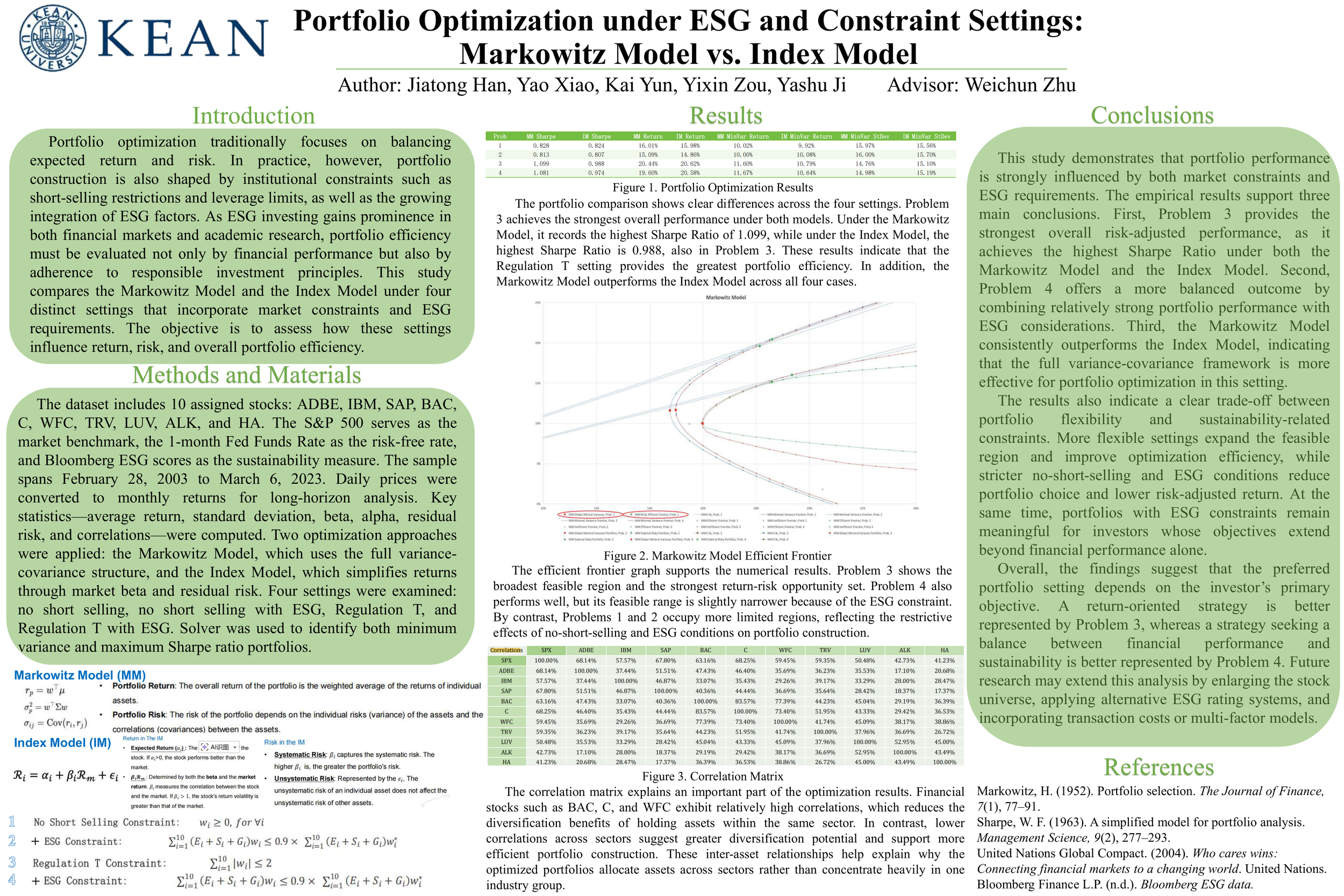

This study is based on modern portfolio theory, employing the Markowitz Mean-Variance Model and William Sharpe's Single-Index Model as the core analytical frameworks to examine the impact of ESG factors on portfolio construction under four constraint conditions.In the data preparation phase, the study selected 10 US-listed stocks from the technology, finance, and industrial sectors. The time is from February 28, 2003, to March 6, 2023, totaling 20 years. The study first obtained daily price data from the Bloomberg database, resampled it to the last trading day's closing price of each month, and then calculated monthly returns. To ensure data stationarity and the validity of statistical inference, monthly frequency was adopted to smooth daily fluctuations and bring the data distribution closer to the conditions of the Central Limit Theorem. Also, the total ESG scores of each stock were obtained from Bloomberg to serve as the basis for subsequent constraint settings.In the statistical indicator calculation phase, the study computed for each stock the annualized average return, annualized standard deviation, Beta coefficient, annualized Alpha, residual standard deviation, and the correlation matrix between assets. The Beta coefficient was calculated using the SLOPE function in regression analysis, reflecting the sensitivity of individual stock returns to market returns. Alpha was obtained by annualizing the regression intercept term, measuring excess returns beyond market explanations. The residual standard deviation measures unsystematic risk, providing the foundation for risk decomposition in the subsequent index model.In the constraint design phase, the study established four progressive optimization scenarios to simulate real investment environments. In the optimization solution phase, the study utilized Excel Solver, with the objective function of maximizing the Sharpe Ratio, to solve for optimal portfolio weights under different constraint conditions, recording key indicators such as optimal weight distribution, portfolio expected return, portfolio standard deviation, and Sharpe Ratio. Simultaneously, by traversing the target return range, the study solved for the minimum variance portfolio at each return level, drawing the complete minimum variance frontier and efficient frontier graphs to visually demonstrate the changing characteristics of the investment feasible region under different constraints.