Assessing the Validity of Likelihood Ratio Tests for Heavy-Tailed Financial Returns

Caleb Wilderotter

Co-Presenters: Individual Presentation

College: Hennings College of Science Mathematics and Technology

Major: BA.MATH/STATS

Faculty Research Mentor: Yousef Nejatbakhsh

Abstract:

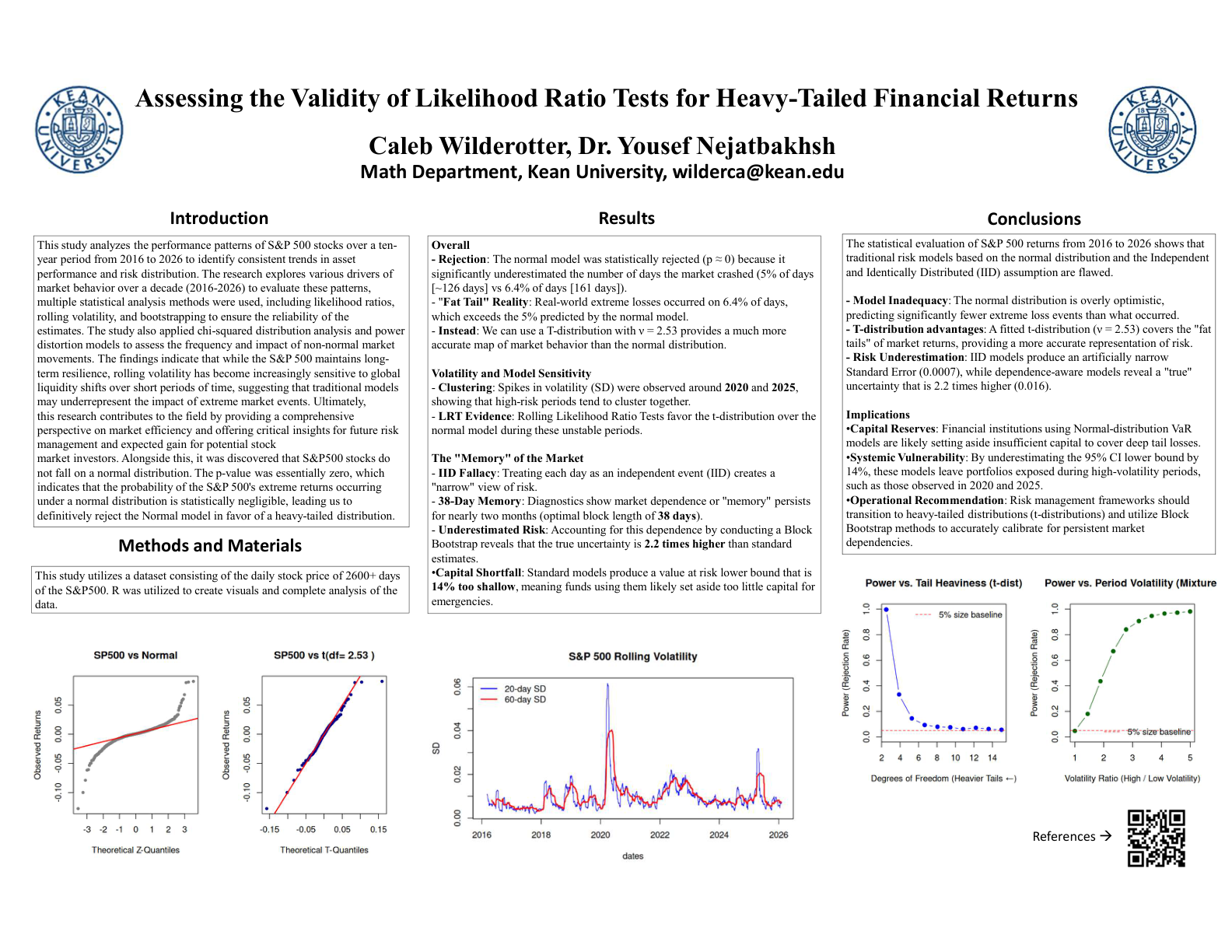

This study analyzes the performance patterns of S&P 500 stocks over a ten-year period from 2016 to 2026 to identify consistent trends in asset performance and risk distribution. The research explores various drivers of market behavior over a decade (2016-2026) to evaluate these patterns, multiple statistical analysis methods were used, including likelihood ratios, rolling volatility, and bootstrapping to ensure the reliability of the estimates. The study also applied chi-squared distribution analysis and power distortion models to assess the frequency and impact of non-normal market movements. The findings indicate that while the S&P 500 maintains long-term resilience, rolling volatility has become increasingly sensitive to global liquidity shifts over short periods of time, suggesting that traditional models may underrepresent the impact of extreme market events. Ultimately, this research contributes to the field by providing a comprehensive perspective on market efficiency and offering critical insights for future risk management and expected gain for potential stock market investors.