Can AI-Managed ETFs Outperform Traditional Factor-Based ETFs?

Afya Prince

Co-Presenters: Emma DiNatale

College: College of Business and Public Management

Major: BS.MANAGEMNT-GENBUS

Faculty Research Mentor: Bo Wang

Abstract:

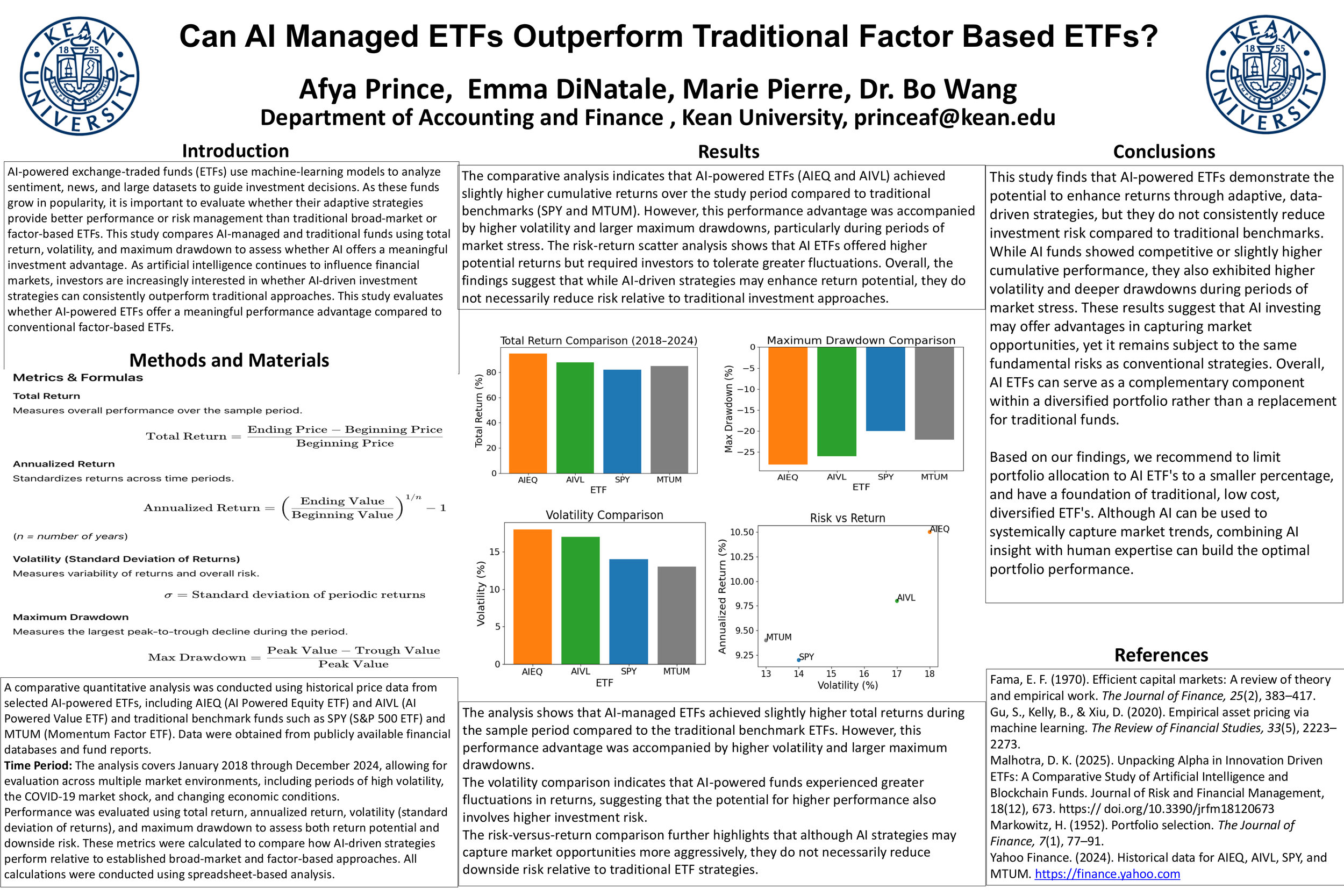

This project examines whether AI‑powered ETFs, which use machine‑learning models to analyze sentiment, news, and large datasets, can match or outperform the results of more traditional factor‑based or broad‑market ETFs. As these AI‑driven funds become more common, investors and researchers are trying to understand whether their adaptive, data‑intensive approach offers a meaningful advantage over long‑established, rules‑based strategies.

The study compares the performance of several AI‑managed ETFs with traditional factor‑based funds across key metrics such as total return, volatility, and maximum drawdown. Because drawdowns reveal how a fund behaves during market stress, they serve as an important test of whether AI models can manage risk more effectively than conventional approaches. The analysis also considers how consistently each type of fund performs across different market environments, including periods of high volatility or rapid shifts in sentiment.

Initial results suggest that AI‑powered ETFs may show bursts of strong performance, especially when markets move quickly and there is value in processing real‑time information. However, factor‑based ETFs often demonstrate steadier long‑term behavior, reflecting their transparent rules and academic foundations. These findings raise broader questions about reliability, interpretability, and whether AI’s flexibility is an advantage or a source of instability.

In general, this research aims to provide a clearer picture of how AI‑managed ETFs compare with traditional investment strategies, helping investors and advisors understand where AI may add value and where established factor models still hold an edge.