Shutdown vs. Debt Ceiling: How Different Political Risks Affect Treasury Bill Volatility

Ziyang Jin

Co-Presenters: Ziyang Jin, Ziteng Wu

College: College of Business and Public Management

Major: BS.FINANCE

Faculty Research Mentor: Ahmed Alam, Eli Kochersperger

Abstract:

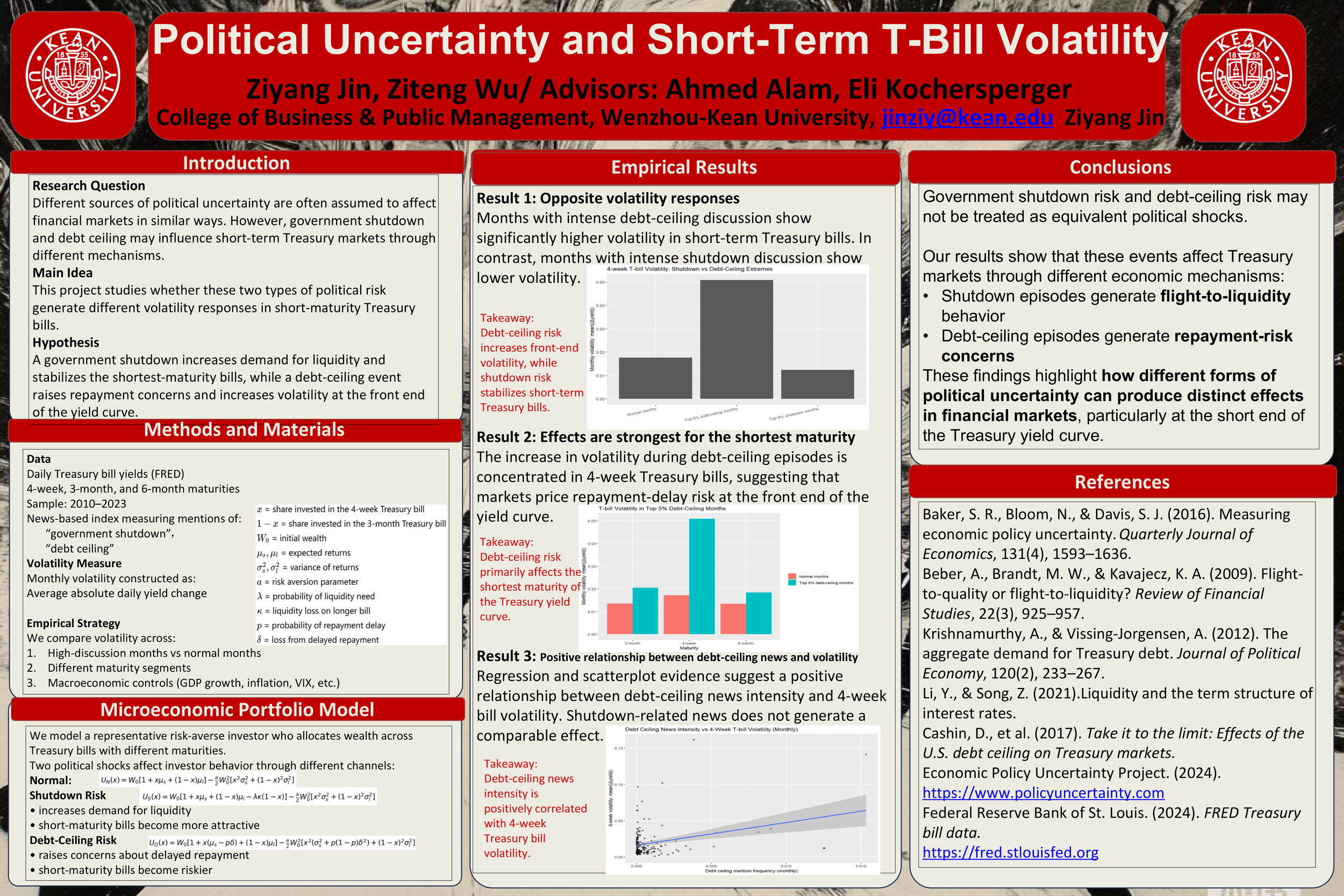

The objective of this study is to determine the effect of political uncertainty on the stability of United States Treasury Bill Markets for securities with short maturities (less than one year), specifically with regard to the fluctuations of yields instead of yield levels. It has been commonly assumed that both government shutdowns and debt ceiling negotiations create similar political uncertainty and therefore impact financial markets through similar mechanisms; however, our research indicates that these two types of political events have different effects and thus will impact T-Bond markets in different ways. Therefore, we develop a framework to study the effects of these two types of events on T-Bond markets using a microeconomic portfolio decision-making framework where risk-averse investors allocate their wealth across T-Bills with different maturities based on a combination of expected return, liquidity, and perception of repayment risk. To create a comprehensive monthly measure of yield fluctuations, we create a composite measure of the daily Treasury Bill rates from the Federal Reserve Economic Data (FRED) (i.e., 4-week, 3-month, and 6-month), combined with a measure of the intensity with which newspapers discuss "government shutdowns" and "debt ceilings". Additionally, we run regression models testing for differences in volatility between heavily discussed months compared to normal months, incorporating controls for lagged volatility, macroeconomic variables (GDP growth, inflation), equity market volatility (EMV), and other measures of uncertainty related to current monetary policy (MPU, TPU). Our findings are that uncertainty created by governmental shutdowns will tend to decrease or stabilize the volatility of 4-week Treasury Bills, due to investment behavior of flight to liquidity, whereas uncertainty created by the Congressional debt ceiling will increase the volatility of 4-week Treasury Bills, due to risk from front-end payments. This study shows how both shutdowns and debt ceilings can result in different variations of short-term Treasury Bonds, which in turn will lead to opposite variations in Treasury Bond market volatility.